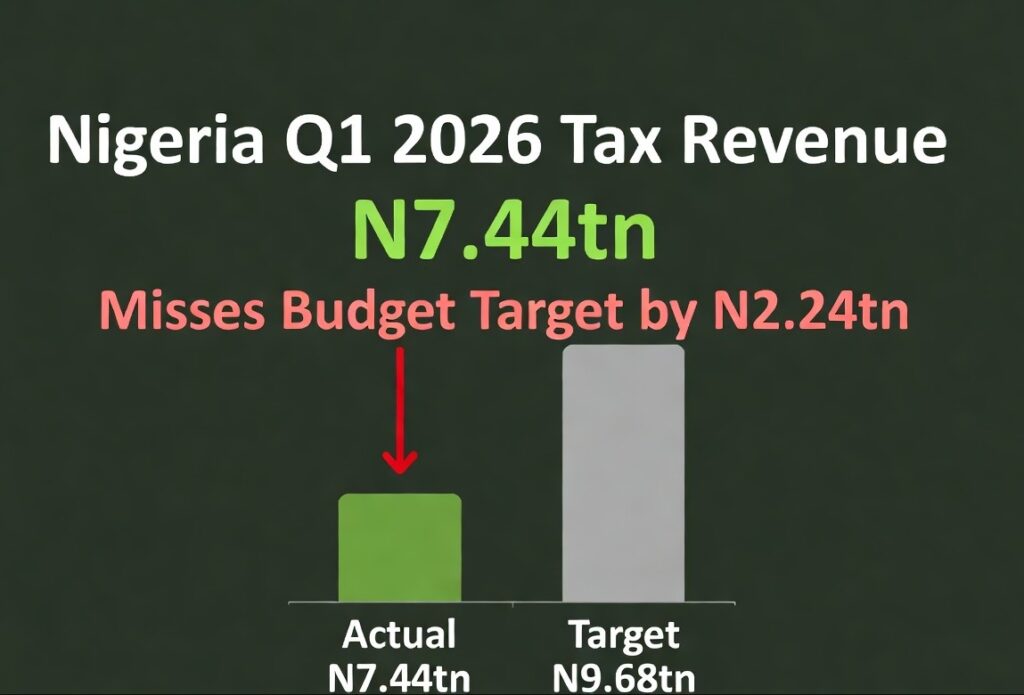

Nigeria Q1 2026 Tax Revenue Hits N7.44tn But Misses National Budget Target by N2.24tn

The newly formed Nigeria Revenue Service faces a steep revenue gap as sweeping tax reforms disrupt corporate filings and trigger strict new FAAC deduction warnings.

Nigeria’s tax revenue collection fell short of its first-quarter budget target by N2.24 trillion in 2026.

The sharp deficit accompanies the rollout of sweeping tax reforms and the operational transition from the Federal Inland Revenue Service (FIRS) to the Nigeria Revenue Service (NRS).

Official documents presented by the NRS at the Federation Account Allocation Committee (FAAC) meetings show that the agency generated a cumulative gross revenue of N7.44 trillion between January and March 2026.

The actual collection stands against a projected quarterly target of N9.68 trillion, representing a performance rate of 76.87 percent.

The current revenue numbers come months after the implementation of the new tax regime which formally transformed the FIRS into the NRS on January 1, 2026.

The performance marks a significantly weaker outing compared to the corresponding period of 2025, when the legacy revenue agency exceeded its first-quarter projections.

FAAC documents from April 2025 showed that the FIRS generated N6.04 trillion in the first three months of last year, surpassing its target by N218.02 billion to post a 103.74 percent performance rate.

While total tax revenue rose year-on-year by N1.40 trillion or 23.16 percent, the growth remained insufficient to meet the aggressive revenue targets embedded in the 2026 fiscal framework.

The Breakdown: Companies Income Tax Drags Down Collections

An analysis of the cumulative quarterly data shows that the largest weakness came from Companies Income Tax (CIT) and related non-oil revenue streams.

The NRS recorded cumulative collections of N3.75 trillion from Companies Income Tax, Capital Gains Tax (CGT), and Stamp Duties against a projected target of N5.05 trillion.

The gap left a substantial deficit of N1.30 trillion and a performance rate of 74.25 percent for the corporate tax category.

The underperformance occurred despite the category generating N2.24 trillion in Q1 2025 and outperforming its target at that time by N218.35 billion.

Companies Income Tax on upstream oil activities also weakened during the first quarter of 2026.

The upstream category generated N349.95 billion against a target of N523 billion, creating a deficit of N173.05 billion and a performance rate of 66.91 percent.

Value Added Tax (VAT) collections remained relatively resilient during the quarter despite missing the baseline targets.

The NRS generated N2.42 trillion from VAT in the first quarter of 2026 against a target of N2.49 trillion, resulting in a modest shortfall of N73.71 billion and a performance rate of 97.04 percent.

The total VAT collection represents a year-on-year increase of 17.06 percent compared to the N2.06 trillion generated in the same period of 2025.

Oil-related taxes recorded the strongest growth year-on-year, driven by changes in international energy prices.

Cumulative collections from Petroleum Profits Tax (PPT) and Hydrocarbon Tax rose to N1.62 trillion from N1.13 trillion in the corresponding period of 2025, representing an increase of 43.66 percent.

The oil tax category exceeded its prorated first-quarter target of N1.30 trillion by N318.23 billion, achieving an overall performance rate of 124.42 percent.

Petroleum royalties and other mineral revenues underperformed significantly, with petroleum royalties alone recording a cumulative shortfall of N909.25 billion after generating N1.12 trillion against a target of N2.03 trillion.

The reports also disclosed that mineral royalties and other mineral revenues failed to record any inflow during the quarter despite a combined quarterly target of N24 billion.

March Revenue Ticks Upward but Misses Monthly Benchmarks

For March 2026 alone, the NRS generated N2.31 trillion against a monthly budget target of N3.23 trillion, representing a shortfall of N915.09 billion.

Despite missing the target, the March figure represented an increase of N120.66 billion or 5.51 percent compared to the N2.19 trillion collected in February 2026.

Oil taxes generated N614.96 billion in March, slightly above the monthly target of N608.75 billion by N6.21 billion.

The agency attributed the slight decline from February oil levels to lower receipts from Production Sharing Contracts (PSCs).

Meanwhile, CIT, CGT, Stamp Duties, and gas income generated N477.54 billion in March, significantly below the monthly target of N1.07 trillion, resulting in a shortfall of N596.62 billion.

The NRS noted that the month-on-month improvement in the corporate category resulted from additional tax remittances received from taxpayers filing returns outside the traditional peak period of June.

VAT collections for March stood at N664.42 billion against a target of N829.92 billion, reflecting a performance rate of 80.06 percent.

The revenue service linked the weaker monthly VAT performance directly to declining consumption of VATable goods in the local market.

The reports further disclosed that the March 2026 gross revenue included non-cash payments worth N294.58 billion and another N24.36 billion embedded in PPT/HCT and gas income collections.

The NRS earlier stated that the new tax reforms position the agency to target an ambitious N40.7 trillion in taxes and royalties for the full 2026 fiscal year.

Executive Chairman of the NRS, Dr. Zacch Adedeji, emphasized that meeting the N40.7 trillion target will require intense compliance efforts across all government and private sector institutions.

NRS Cautions States: Unremitted Taxes to Trigger Direct FAAC Deductions

The NRS has warned states, ministries, departments, and agencies (MDAs) that unremitted taxes will now trigger direct deductions from their FAAC allocations.

The warning was issued in Abuja by the Executive Director of the Government and Large Taxpayer Directorate at the NRS, Amina Ado, during a national workshop on tax compliance.

Ado stated that the Nigerian Tax Administration Act has embedded automated enforcement mechanisms directly into the national fiscal system.

“Unremitted revenue can be deducted from allocations,” she warned during the workshop presentation.

Section 80 of the Act empowers the Accountant General of the Federation to deduct all unremitted revenues due from any MDA or government from its budgetary allocation.

The deducted funds will be remitted directly to the relevant tax authority, whether federal or state, after a specific due process has been followed.

Ado emphasized that withholding and remittance obligations must now be treated as “allocation protection activities” by state governments.

If a federal, state, or local government treats withholding tax as someone else’s responsibility, the law provides a mechanism for that neglect to return immediately through deductions from allocations.

Field monitoring and audit activities by the NRS have uncovered structural leakages in the deduction and remittance of VAT and Withholding Tax (WHT) by some government institutions.

The agency noted that the imbalance distorts fiscal federalism because some states contribute significantly to the national revenue pool while others mainly participate in the sharing process.

Under Section 155 of the Nigerian Tax Act, all levels of government and their agencies are mandated to collect or withhold VAT on taxable supplies and remit it to the NRS on or before the 14th day of the following month.

All ministries, departments, agencies, and local governments are now required under the law to register for tax and obtain individual Tax Identification Numbers (TINs).

Section 72 of the Nigerian Tax Administration Act also makes valid tax clearance certificates mandatory before any contractor can enter into agreements with public institutions.

The Minister of Finance and Coordinating Minister of the Economy, Taiwo Oyedele, stated that the new tax framework aims to expand the tax net without increasing the tax burden.

Accountant-General of the Federation, Dr. Shamseldeen Ogunjimi, added that stronger intergovernmental cooperation and digitalization are critical to improving compliance and collections.